When asking how much does alcohol detox cost, many people are discouraged by seeing extremely high figures online. In reality, the cost of detox varies based on the level of care, length of treatment, medical needs, and insurance coverage.

A medically supervised alcohol detox program typically costs between $1,000 and $7,000 out of pocket, with most programs lasting 5 to 14 days. Inpatient detox generally costs more than outpatient care, and daily rates often range from $250 to $800, depending on the services provided. While luxury facilities may charge significantly more, these figures represent a more typical range for medically supervised detox programs.

Kora Behavioral Health alcohol detox may be more affordable than many people expect. Most private insurance plans, employer-sponsored coverage, and many Medicaid plans include benefits for medically necessary alcohol detox, which can significantly reduce out-of-pocket costs. Because alcohol withdrawal can involve serious medical risks, detox is often recognized as a medically necessary service when appropriate.

While no provider can quote an exact cost without reviewing your insurance benefits and clinical needs, understanding how coverage works can make the process less overwhelming. This guide explains the factors that influence detox costs, how insurance benefits are applied, and what options may be available if you are underinsured or paying out of pocket.

What Drives Alcohol Detox Cost?

When considering alcohol detox cost with insurance, it’s important to understand that pricing varies based on medical needs, the level of care required, and your insurance benefits. Even with coverage, out-of-pocket costs can differ depending on factors such as deductibles, copays, coinsurance, and whether the treatment facility is in-network.

One of the biggest cost factors is the complexity of alcohol withdrawal itself. Because severe withdrawal can lead to serious complications—including seizures and delirium tremens—some individuals require intensive medical monitoring, medications, and around-the-clock clinical care. Those additional services increase the overall cost of treatment but are often medically necessary to ensure a safe detox process.

The factors that push costs up or down include how severe your physical dependence is, how long you’ve been drinking at what volume, whether you have co-occurring medical conditions like liver disease or hypertension, what medications are needed to manage withdrawal safely (benzodiazepines like lorazepam or diazepam are standard, but medication protocols vary), and whether lab work, EKG monitoring, or specialist consultation gets added to your clinical picture.

Geographic location matters too. A detox stay in suburban Pennsylvania is priced differently than one in Manhattan or rural Montana. Facilities in higher cost-of-living markets carry higher overhead, and that gets passed to the patient.

| Cost Factor | May Increase Cost? | Why |

| Inpatient vs. outpatient setting | Yes (inpatient) | 24/7 nursing, housing, meals included |

| Withdrawal severity | Yes | More medication, monitoring, possible ICU escalation |

| Length of stay | Yes | Longer detox = more daily charges |

| Geographic location | Yes (urban markets) | Higher operational overhead |

| Co-occurring medical conditions | Yes | Additional labs, specialist consults |

| Luxury amenities | Yes | Private rooms, premium services, branding |

| Insurance coverage | No (reduces cost) | Shifts financial responsibility to insurer |

Why Two People May Pay Very Different Amounts

Insurance is the biggest variable of all, honestly. Two people can walk into the same facility with the same diagnosis and end up with completely different bills — one pays a $500 deductible, the other gets a $4,000 invoice — purely because of how their individual plan is structured. Beyond that, clinical complexity shapes the level of care recommended, and the level of care recommended shapes the price. Someone with mild-to-moderate physical dependence and no significant medical history is a different case than someone with a decade of heavy daily drinking and compromised liver function.

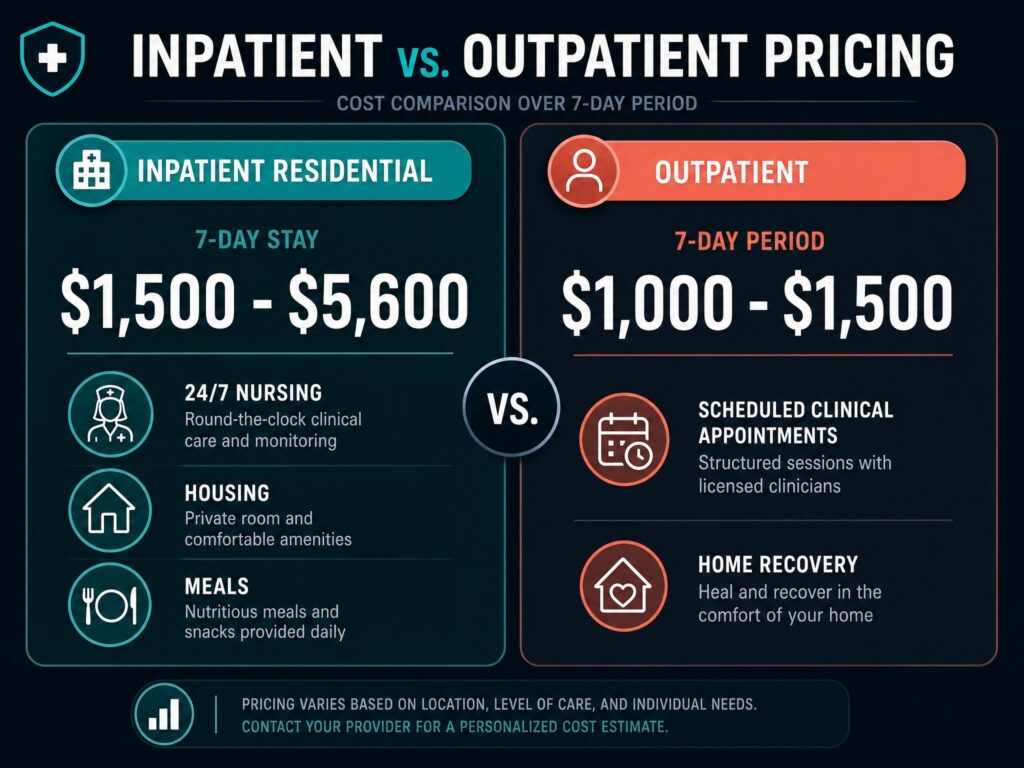

Inpatient vs. Outpatient Pricing

The setting you detox in is the single biggest cost lever in the whole equation.

Inpatient residential detox — where you stay at a licensed medical facility around the clock — runs roughly $1,500 to $5,600 for a seven-day stay, with an average somewhere near $3,675 based on current national pricing data. The daily rate typically falls between $250 and $800. That price point reflects actual services: physician-led medical oversight, nursing assessments every few hours, medication administration, vital sign monitoring, meals, and a controlled environment that removes access to alcohol entirely. Luxury or private-suite facilities charge more — often $500 to $650 per day or higher — but fancier accommodations don’t automatically translate to better clinical outcomes for most people.

Outpatient detox is significantly less expensive, typically totaling between $1,000 and $1,500 for the full program. Patients attend scheduled clinical appointments, receive medication and monitoring during those visits, and go home between sessions. The lower cost reflects what’s absent: no overnight staffing, no housing, no around-the-clock nursing. For individuals with mild-to-moderate alcohol dependence and a stable home environment, outpatient detox can be medically appropriate and genuinely effective.

Why Cheapest Isn’t Always Safest

Here’s what I’d want someone I care about to understand: alcohol withdrawal has a mortality risk that other substance withdrawals simply don’t. Delirium tremens carries an untreated fatality rate that’s been documented in clinical literature for decades. The clinical practice guidelines from ASAM on alcohol withdrawal management exist precisely because this is a condition that requires physician oversight, not willpower. Choosing a lower level of care than your medical picture actually warrants — because it costs less — is one of the few situations where cost-cutting can have genuinely serious consequences. That determination should always come from a clinical assessment, not from a pricing comparison.

How Insurance Coverage Works for Detox

Under the Affordable Care Act, substance use disorder treatment is classified as an essential health benefit. That legal designation matters because it means most insurance plans sold through the marketplace, as well as employer-sponsored plans, are required to cover it. For medically supervised alcohol detox, the practical effect is that coverage is available — the question is how much of the bill your specific plan absorbs versus what falls to you.

The way insurers evaluate a detox claim typically involves a few core criteria: your documented diagnosis (Alcohol Use Disorder, using DSM-5 criteria), your clinical withdrawal risk score (tools like CIWA-Ar are standard), the treating clinician’s recommendation for level of care, and whether the requested setting is consistent with evidence-based guidelines. When those boxes are checked, prior authorization — when required — usually isn’t the battle people fear it will be.

What you actually pay out of pocket depends on your plan’s deductible (the amount you owe before insurance kicks in), your copay or coinsurance rate (your percentage of costs after the deductible), and whether you’ve already met any of your out-of-pocket maximum for the year. If you’re later in a calendar year and you’ve already accumulated medical expenses, you might find detox costs almost entirely covered.

What Insurance Usually Reviews

When a utilization review team at an insurer evaluates a detox authorization, they’re primarily looking at your withdrawal severity and the clinical justification for the level of care being requested. A mild CIWA score probably supports outpatient. A high score, combined with a history of prior seizures or complicated withdrawals, strongly supports inpatient medical detox. The clinical documentation your treatment team submits directly influences what gets approved and at what level.

Quick Insurance Glossary:

- Deductible: What you pay before insurance begins sharing costs

- Copay: A fixed fee per service or visit

- Coinsurance: Your percentage share of costs after the deductible

- Out-of-pocket maximum: The most you’ll pay in a plan year; after this, insurance covers 100%

- Prior authorization: Insurer pre-approval for certain services before treatment begins

In-Network vs. Out-of-Network

This distinction probably causes more financial surprise than anything else in the treatment system. When a facility is in-network with your insurance plan, the insurer and that provider have a negotiated rate agreement. You pay your standard cost-sharing amounts. When a facility is out-of-network, those negotiated rates don’t apply, your plan may cover a much smaller percentage of costs, and you could face balance billing for the difference between what the insurer pays and what the facility charges.

Verification before admission isn’t just a formality. It’s genuinely the step that determines whether you’re walking into a situation where insurance covers 80% of your costs or a situation where you’re personally on the hook for a bill that arrives six weeks later.

Major Pennsylvania Insurers and Detox Coverage

Pennsylvania residents have access to a fairly robust network of coverage options for substance use treatment, including Medicaid managed care through Commonwealth programs, as well as major commercial carriers like Highmark, UPMC Health Plan, Aetna, Cigna, and Blue Cross Blue Shield of Pennsylvania. Most of these plans offer substance use disorder benefits aligned with ACA requirements, but — and this matters — coverage terms vary substantially between individual plan tiers, even within the same insurance company.

An employer-sponsored Highmark plan and an individual marketplace Highmark plan can have completely different deductibles, different prior authorization requirements, and different in-network provider lists. The insurer name alone tells you almost nothing. Your specific plan documents tell you everything. If you’re unsure what your benefits actually cover for alcohol detox in Pennsylvania, the only reliable way to find out is to verify directly through your insurance benefits portal on healthcare.gov or by calling the facility’s admissions team.

Options if You’re Underinsured or Uninsured

I want to be honest about something here: the gap between “insurance should cover this” and “insurance is actually covering this right now for you” can feel enormous when you’re in crisis. The system is not graceful about delivering help quickly to people who need it most urgently.

That said, options do exist, and they’re worth exhausting before assuming treatment is out of reach:

- State-funded treatment programs through Pennsylvania’s Single County Authorities (SCAs) can cover detox costs for qualifying residents, and eligibility isn’t strictly limited to people with zero income.

- Sliding scale fees at nonprofit and community-based facilities adjust cost based on your financial situation.

- SAMHSA’s National Helpline and treatment locator connects people with free or low-cost local options, often the same day.

- Open enrollment periods or qualifying life events can make you eligible for marketplace coverage — worth checking even if you’re mid-year.

The instinct when you see a large price tag is to self-eliminate before anyone even reviews your situation. Don’t. Admissions teams at legitimate facilities work through financial questions regularly. A conversation costs nothing.

How to Verify Your Benefits Fast

If you’re wondering, does insurance cover alcohol detox, verifying your benefits is usually much simpler than most people expect. In most cases, you only need your insurance card and a few minutes to speak with an admissions coordinator.

At Kora Behavioral Health alcohol detox, an admissions coordinator can verify your insurance benefits by contacting your insurer to confirm coverage for medically supervised detox, explain your deductible and estimated out-of-pocket costs, and determine whether prior authorization is required. This process is confidential, does not obligate you to begin treatment, and does not create a treatment record. Most importantly, it replaces uncertainty with clear information, allowing you to make an informed decision about your next steps.

Verify Your Insurance Coverage in Minutes — Free & Confidential Call (866) 861-9667

FAQs

Does insurance cover alcohol detox?

Many insurance plans do cover medically necessary alcohol detox, including most plans sold through the ACA marketplace and employer-sponsored coverage. The Affordable Care Act classifies substance use disorder treatment as an essential health benefit, which obligates most plans to include it. The coverage amount — meaning what you personally pay — depends on your specific plan’s deductible, coinsurance rate, and whether the facility is in-network. Coverage isn’t automatic or uniform across every plan, which is why benefit verification before starting treatment is always the recommended first step.

How much is detox without insurance?

Without insurance, out-of-pocket costs for a standard alcohol detox program typically range from $1,000 to $7,000, with daily rates running $250 to $800 depending on setting and medical intensity. Inpatient residential detox costs more than outpatient because it includes around-the-clock medical staffing, housing, and meals. Luxury programs can run significantly higher. State-funded programs, sliding scale facilities, and nonprofit options can reduce or eliminate cost for qualifying individuals — so the self-pay figures above represent private-pay pricing, not the full picture of what’s accessible.

Which insurers cover detox in Pennsylvania?

Most major commercial insurers operating in Pennsylvania — including Highmark, UPMC Health Plan, Aetna, Cigna, and Blue Cross Blue Shield of Pennsylvania — offer plans that include substance use disorder benefits. Pennsylvania Medicaid (Medical Assistance) also covers medically necessary detox for eligible residents. The critical caveat is that coverage terms vary by individual plan, not just by insurer. Two people with Highmark insurance can have meaningfully different benefits. The only way to know what your plan actually covers is to verify your specific benefits, either through your plan documents or directly with a provider’s admissions team.